Cost

reduction, optimization, management

Strengthen your competitiveness with us

Cost reduction, optimization, management

Strengthen your competitiveness with us

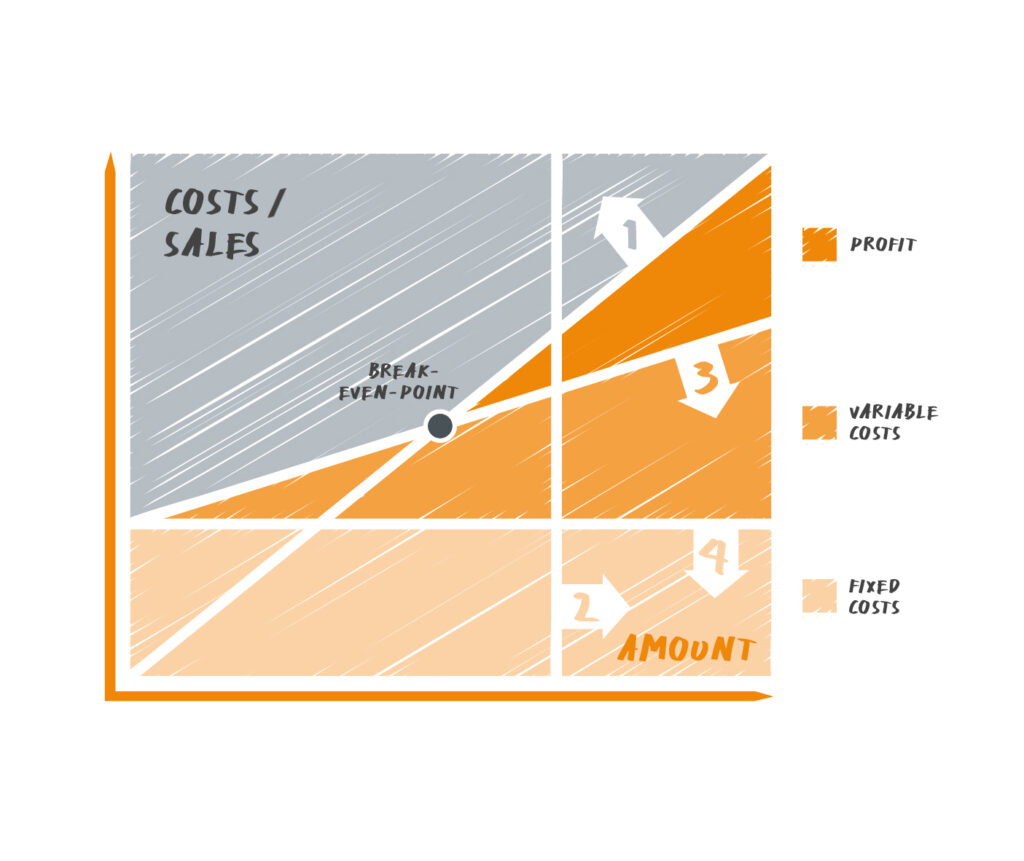

If companies are talking about cost reduction, they generally refer to the areas of product cost reduction and overhead cost reduction. The cost items in a company reflect the use of resources. Material prices, salaries, and wages as well as an increasing number of laws and market regulations to be fulfilled increase costs without your company being able to influence them.

This is problematic, because the resulting cost increases can rarely be passed on to your customers in full. This not only has a direct impact on your profit, but also threatens your competitiveness!

It is therefore important to identify those cost items which can be reduced by active, internal company measures. This is where we come in.

Our service

- Analysis of the overall cost situation

- Determination of requirements

- Identification of cost units & division into controllable and non-influenceable cost items

- Function analysis

- Calculation of accepted costs per function

- Developing measures to close the gap between existing and accepted costs

- Support of the implementation until success is achieved

Your value

- Sensitization of all parties involved to the economical use of costs

- Reduction of variable product costs between 5-40%

- Reduction of overhead costs between 10-25%

- Implementation of an entrepreneurial view on direct and indirect costs as a basis for sustainable decisions

- Increased competitiveness (in the international environment)

Are you interested in a first consultation or do you have any questions about cost reduction?

Reduce product costs and increase customer benefit

The competitiveness of a company depends strongly on the competitiveness of its products and services. Competitiveness is achieved by continuously maintaining the products in the product portfolio.

When maintaining the products, the customer benefit is to be questioned cyclically and improved, if necessary, and the costs of creating the products are to be worked on. Increasing competition is driving manufacturing companies ahead and putting pressure on prices.

A holistic approach is needed to master the emerging challenges. The manufacturing costs, which are made up of material and production costs, must be analysed in their entirety and worked on for reduction potential. Value Analysis / Value Engineering is known to be an effective methodology for this purpose.

Reduce overhead costs and regain innovative ability

The overhead cost areas have expanded almost unnoticed in recent years and represent a significant potential for cost reduction and margin improvement.

Reasons for the increase in overhead costs may be:

- Increased administrative expenses in almost all corporate divisions, e.g. due to the expansion of the product range and compliance with a wide range of regulations,

- Expansion of the sales units to serve the globalized markets,

- International networking and thus complex project organizations.

The increase in overheads has also led to companies becoming inefficient and sluggish.

As a result:

- Fast reactions to market changes are difficult,

- new technologies find their way too slowly into our own products and

- there is a lack of ideas for new products and innovations.

Such a challenging task to massively reduce overhead costs can be advantageously handled by appropriate methodical procedures. Krehl & Partner also uses the application-neutral methodology of Value Analysis / Value Engineering for this purpose.